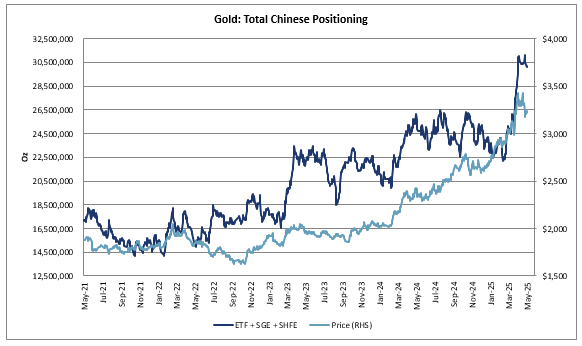

Gold is getting a big boost from Chinese investors once again, and mainland demand is helping to push the yellow metal closer to last month’s all-time highs as all levels of the Chinese system appear to be banking on bullion for the long haul.

The latest customs data released Tuesday showed China imported more gold last month than they had in nearly a year, and this despite bullion prices setting a new historic high of $3,500 per ounce in April.

Total gold imports reached 127.5 metric tonnes last month, an 11-month high, and represented a 73% rise from March’s figure, even though gold prices were in uncharted territory at the time.

The surge in gold imports was due in part to the People’s Bank of China (PBoC) issuing additional import quotas to some commercial banks in April, as the central bank was compelled to respond to strong demand from institutional and retail investors at what proved to be the peak of U.S.-China trade war anxiety.

And momentum is not slowing. The Chinese gold market has continued to support gold prices this month. Following weeks of uncharacteristic weakness, it was Chinese investors who once again stepped in to buy up the yellow metal as it languished at multi-week lows, with bullion prices now trading back above $3,300 per ounce.

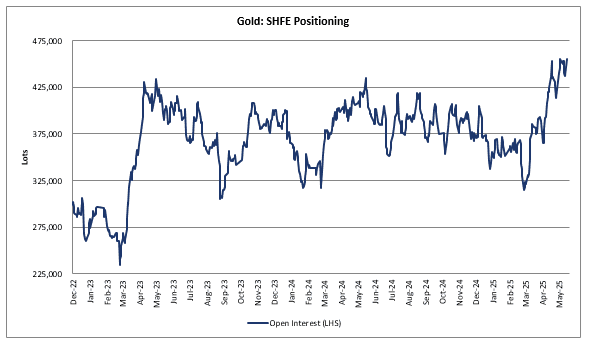

“According to Goldman’s flow tracker, Shanghai’s night session has come alive, triggering a classic COMEX sympathy bid,” wrote Stephen Innes, Head of Trading and Market Strategy at SPI Asset Management on Wednesday. “Open interest on SHFE is back at all-time highs, with gold and silver both seeing a sharp jump—+3% and +4%, respectively.”

“That kind of synchronized positioning doesn’t happen by accident,” he added.

Innes said what’s even more telling is the resilience of domestic Chinese traders. “Despite the 8% drawdown from the recent peak, they held their fire, refusing to dump positions,” he said. “That’s not momentum chasing—that’s conviction. And when the SGE/LBMA arb lit up, global buying interest reignited.”

He also noted the one-year high in imports, saying, “It means the physical premium on the Shanghai Gold Exchange (SGE) isn’t just holding up, it’s punching through resistance.”

“And the market setup is clean,” Innes pointed out. “Ex-China hedge fund positioning is light, and CFTC data shows specs are flat, not leaning long. That makes the skew look dirt cheap—6-month 25-delta risk reversals are trading around 2.25v, with 6m implied vols near 19.5%. I think you want to own that optionality—vol should outperform if we break new highs, and the vanna tailwind is real.”

The bottom line, Innes said, is that this is far more than a bounce. “This is a reset,” he said. “The physical bid from China, the clean slate in Western positioning, and the quietly persistent vol buyers all suggest one thing: The gold bull isn’t dead—it was just consolidating. And the dragon just hit the buy button again.”

And while U.S.-China trade tensions have eased in the near term following the recent Geneva trade agreement, China is continuing to leverage gold to fulfill its long-term de-dollarization goal.

“As global power dynamics shift, China is steadily advancing a long-term financial strategy aimed at reshaping the international monetary order,” wrote Charles-Henry Monchau, Chief Investment Officer at Syz Group. “Central to this effort is a decisive move away from the US dollar, a currency that has dominated global trade, reserves, and finance for nearly a century. In its place, China is betting on a dual foundation: gold and the yuan.”

Monchau said China’s gold strategy is primarily a pragmatic one. “Holding trillions in dollar-denominated assets has long made China vulnerable to US financial pressure, sanctions, and market volatility,” he said. “By accumulating massive gold reserves and quietly internationalising the yuan through initiatives like the Shanghai Gold Exchange, Beijing is building a parallel financial architecture, one that enhances its autonomy while reducing exposure to the dollar-centric system.”

He refers to China’s approach as “calculated, gradual, and deeply strategic. Gold serves not only as a hedge against currency risk but as a symbol of monetary sovereignty. Meanwhile, the yuan, still constrained by capital controls, is gaining legitimacy through trade and bilateral agreements. Together, gold and the yuan are emerging as pillars of a broader Chinese ambition: to assert greater influence in global finance on its own terms.”

Monchau also noted that many analysts believe China’s real gold holdings are far larger than the official numbers. “Reports suggest the People’s Bank of China (PBoC) may be buying five times more gold than it discloses to the IMF, with real reserves potentially surpassing 5,000 tons,” he said. “This opacity is deliberate—by quietly shifting reserves from dollars into gold, China avoids alarming markets while progressively building leverage.”

“What makes this strategy effective is its subtlety,” he said. “Unlike dumping Treasuries, which could trigger market panic and backfire economically, buying gold is a quiet, cumulative tactic. It exerts downward pressure on the dollar over time, especially if other nations follow suit. By transforming some of its surplus dollars into gold, China reduces global demand for the greenback while building a monetary buffer that reflects real value.”

Monchau characterizes this strategy as “not a revolution, but a rebalancing.”

“Through calculated gold accumulation and the slow elevation of the yuan in global trade, Beijing is building leverage, not detonating it,” he said. “The aim is not to topple the dollar overnight, but to reduce exposure, hedge against financial coercion, and quietly offer the world another option.”

“The world may not be ready to abandon the dollar, but it is increasingly prepared to consider alternatives,” Monchau concluded. “As inflation, sanctions, and debt reshape global finance, China’s gold-and-yuan strategy positions it not just as a rival to US economic power, but as an architect of the next monetary era, a system less reliant on trust and more grounded in value.”

.png?width=1500&height=626&name=Copy%20of%20GIF%20HEADER%201%20(1).png)